Since our listing, as a company which continuously conducts M&A while adhering to Japanese GAAP (JGAAP), we have made efforts to enhance our disclosures.

Specifically, we have (1) indicated cash flow indicators and (2) shown intrinsic performance excluding one-off M&A costs.

Regarding (1), we have shown earnings that indicate cash flow before “goodwill amortization expense” is deducted, because under Japanese GAAP (JGAAP), goodwill amortization expense, which has no cash outflow, is recorded as a cost.

For (2), we have been presenting “adjusted” profit indicators, which are indicators calculated before the deduction of one-off costs such as M&A fees, etc., in order to show the true performance of our existing businesses.

However, we have received comments that the additional disclosure of the above indicators has resulted in excessive and complicated information.

Therefore, we have decided to narrow down our presentation to the following KPI indicators to show our actual earning capacity, while taking into account (1) and (2) again.

- Revenue

- Adjusted EBITDA

- Adjusted net income (The current “Adjusted net income before amortization of goodwill” will be referred to as “Adjusted net income”)

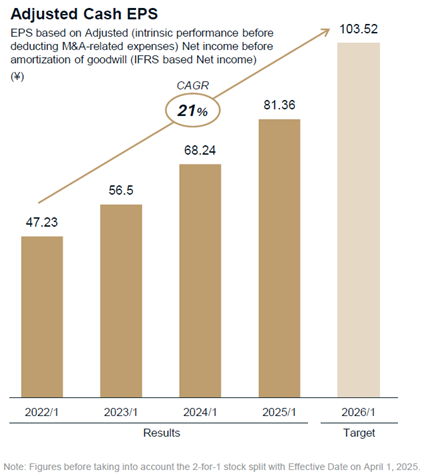

- Adjusted EPS (The current “Adjusted Cash EPS” will be referred to as “Adjusted EPS”)

About i.ii.iii.

Beginning with the next fiscal year (ending on January 31, 2027), we will only disclose these three indicators in the company’s earnings forecast at the beginning of the fiscal year. Until the current fiscal year, we have not been able to incorporate the current performance into our forecasts because we could not predict whether there would be any one-off expenses from M&A during the fiscal year. Starting next fiscal year, by using only the adjusted KPI indicators in our forecasts, it will become unnecessary to predict the presence or absence of one-off expenses from M&A activities during the fiscal year, thereby allowing us to reflect our current business performance in the earnings forecast.

In addition, considering the introduction of IFRS from the end of the next fiscal year, the company’s forecasted net income will be closer to the IFRS net income excluding amortization of goodwill, which will bring the P/E multiple of the company’s forecast closer to the IFRS standard.

About iv.

As an M&A company, we also believe that it is natural for the company’s sales and earnings to increase in a transformational way as a result of the consolidation of the earnings of newly consolidated companies.

On the other hand, in our M&A activities, there is also an increase in the number of shares due to stock deal M&A and follow-on offerings. Therefore, it is important to show whether earnings growth exceeds the increase in the number of shares and leads to an increase in EPS, the value per share.

Conversely, we believe that no matter how much earnings increase, if the number of shares increases more than that, it is not growth. Based on this, we also use adjusted EPS as a KPI.

For your reference, the following is an excerpt from a past presentation showing our adjusted EPS transition (current adjusted Cash EPS).

(Reference: page 11 of “M&A Announced today” disclosed on April 9, 2025)

This presentation was prepared prior to the follow-on offering conducted last May, but by utilizing all of the funds raised through that offering for M&A, we aim to maximize our Adjusted EPS starting from the fiscal year ending on January 31, 2027.