As you point out, if our growth through M&A could be achieved entirely through debt financing alone, earnings per share would increase more.

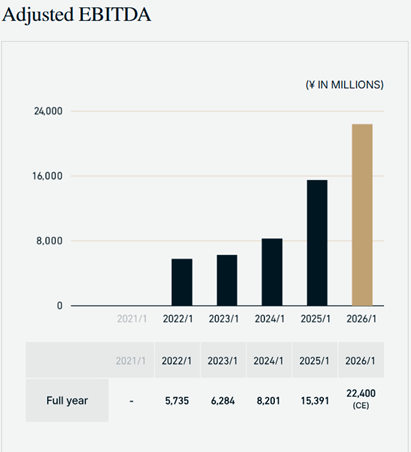

However, unfortunately, it is not realistically feasible to achieve the growth in EBITDA of 8.2 billion yen → 15.3 billion yen → 22.4 billion yen … only with debt.

Growth with “debt financing only + no equity financing” will be a huge opportunity loss for our earnings per share. This is because we are unable to conduct M&A without financial soundness in the first place, however, if we maintain financial soundness without making an offering, we will lose a great opportunity for executable M&As.

On the other hand, with “no debt financing + equity financing only,” it would not lead to the same growth in earnings per share as described above.

What this suggests is not a dichotomy of “debt financing or equity financing,” but it is possible to make a design which keeps growing while maintaining an optimal balance between the two.

That is “to finance maintaining good balance between borrowing and offering to the extent that earnings per share (significantly) increases.”

The key for that scheme is a capital structure that “adding a unit of equity capital (offering) expands Debt Capacity by a larger scale.”

This means that significant debt capacity becomes available only after our capital base is strengthened through an equity offering, and as a result, the total amount of funds which can be raised increases, the available amount for M&A increases and the earnings to be consolidated through M&A will increase subsequently.

This is a cycle that earnings per share increase if the increase in earnings consolidated through the M&A exceeds the increase in the number of shares through an equity offering. We have consistently achieved this through the aforementioned leverage effect since our establishment, with an EPS growth rate (CAGR) of +21% over the past five years, a forecast EPS growth rate (pre-offering basis) of +27% for the current fiscal year (ended January 31, 2026), and an EPS growth effect from the this follow-on offering of +41% if the underlying assumptions hold.