We refrain from making an official comment regarding the validity of the stock price, as we are not allowed to do so as a listed company. On the other hand, it is possible for us to explain the structure of the stock price formation and organize the facts, and explain the inferences based on them.

Although there are multiple methods for calculating stock price, one of the general formulas is “stock price=EPS × P/E multiple.”

As for “EPS,” we can actively improve it through corporate efforts, and in fact, it has grown substantially since the last equity offering, and we will also invest the funds raised through this offering to lead to further growth, as mentioned earlier.

On the other hand, we do not have complete control over “P/E multiple” as it is based on the macro stock market environment and our specific investors’ forecast for the growth in our EPS. Therefore, regarding P/E multiple, we will first organize objective facts and then describe our observations.

As a fact, our P/E multiple is currently around 20x, the lowest level since our listing (P/E multiple is based on the forecast net income on IFRS-basis (= net income before amortization of goodwill) for this fiscal year, 8.0 billion yen). Next, the time series of changes in P/E multiple until today is as follows;

- ~3/24 Since the announcement of financial results and new structure on March 12, the stock price had been close to historical high, and P/E multiple was 29x

- 3/25 Started falling due to US media reports on the Trump administration’s tariffs against China

- 4/8 Kept falling after Trump administration tariffs against China at 104%,

- 4/9 Temporarily rebounded with our largest ever M&A in North America (Player One)

- 4/10 Fell again with Trump administration tariffs against China at 145%

- 5/1 Temporarily rebounded after Tokai Tokyo Securities Co., Ltd. had issued an analyst report

- 5/13 Fell again as we announced a follow-on offering + secondary offering

- 5/30 P/E multiple is about 20x as of today, down approximately -35% since the announcement of financial results and the new management, the lowest level since listing

On May 12, there was good news that tariffs against China would be reduced to 30%. However, the timing of announcement of M&A with Player One coincided with reports of tariffs against China, which added to concerns about the offering and limited the impact on P/E multiple.

Next, as of today, although the tariff issue between the U.S. and China, which is a macro factor, temporarily settled and the concerns about the follow-on offering were dispelled, P/E multiple still remains at the lowest level since listing.

What we can see from this is that it is considered that the market may have become more skeptical about the growth potential of our EPS than before.

In addition, since the use of the funds raised this time is for M&A as well as last time, it is difficult to disclose in advance the explicit use of the funds, as is the case with organic growth, and we believe that further confidence from the market will be required for the growth potential of EPS in the future.

Besides, we recognize that the partial sale of equity by Shin, who is the former Representative Director and President of the Company and currently serving as a Director, has attracted a certain amount of attention in the market.

On the other hand, let us explain that our medium- to long-term growth strategy remains unchanged as follows.

First, the indicators that we have published are as follows.

- In the long term, we aim to be the world’s No. 1 entertainment company in 2040.

- In the medium term, we aim to fulfill the conditions for exercise of stock acquisition rights, 75.0 billion yen in EBITDA in 2030.

The incentives owned by our officers and employees are stock acquisition rights, which directly motivate them to increase the stock price itself, rather than just market capitalization. Since the stock price generally consists of “stock price = EPS x P/E multiple,” we will stubbornly focus on the growth in EPS, which is controllable.

P/E multiple, whose simplified theoretical formula is “P/E multiple = 1 ÷ (weighted average cost of capital – EPS growth rate),” clearly indicates that sustained EPS growth is extremely important for P/E multiple.

In this regard, our growth in EPS is robust although our mainstay is M&A:

- EPS growth rate (CAGR) for five years from FY2022/1 to FY2026/1 (forecast) is +21%

- EPS growth rate (pre-offering basis) from FY2025/1 to FY2026/1 (forecast) is +27%

- EPS growth effect through this follow-on offering, assuming that the assumptions remain unchanged, is +41%

To summarize, based on the fundamental equation: Share Price = EPS × P/E multiple our current position and future direction can be outlined as follows:

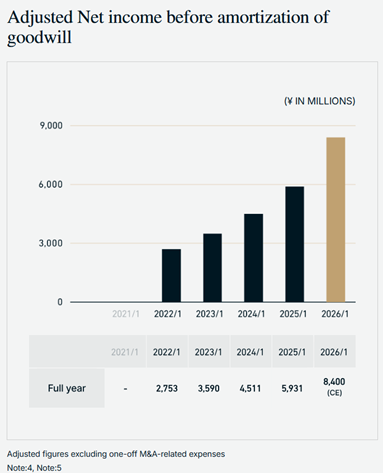

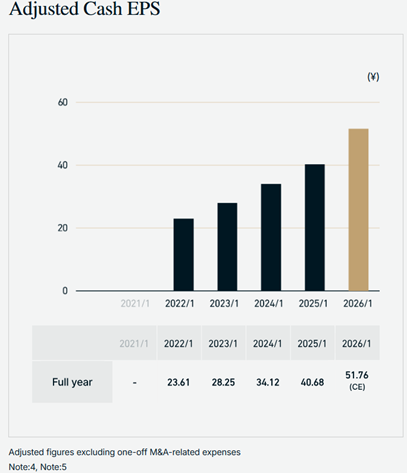

- “EPS” has reached an all-time high, as shown in the chart below

- “EPS” has no upper / lower limit, and we are aiming to continuously setting new records from 2025 to 2030 to 2040.

- “P/E multiple” tends to fluctuate within a certain range, due to market arbitrage relative to alternative investment opportunities.

- “P/E multiple” is currently near all-time low.

Given above, the key to factor of P/E multiple lies in how much EPS growth are expected from the market. We will remain committed to proactive and transparent dialogue with the capital markets.