To summarize our position: there is absolutely no change to the core of our strategy – achieving “Transformational growth through continuous M&A” – nor to our discipline of pursuing “M&A that contributes to EPS improvement.”

Building on this foundation, we have announced a “shift toward an M&A strategy aligned with the capital markets,” and have committed to not conducting any “public offerings for the purpose of securing M&A standby funds” until at least the end of January 2029.

(Source: page 6 of “FY2026/1 3Q Earnings Presentation” disclosed on December 12, 2025)

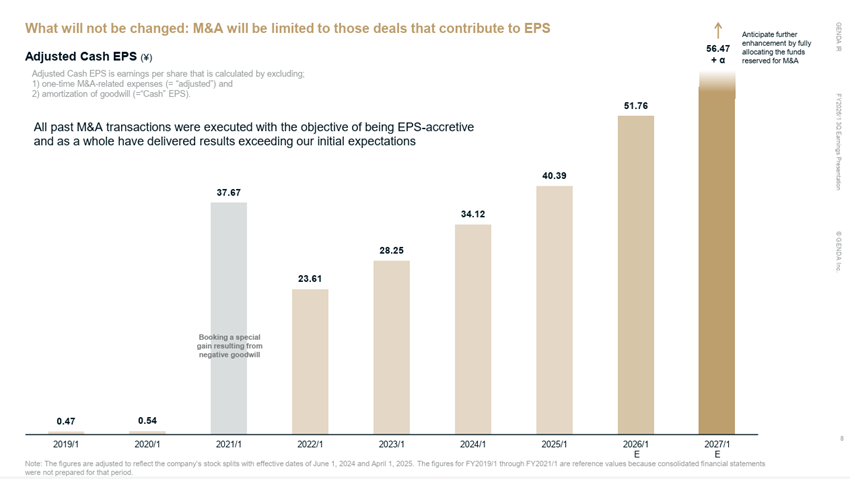

Since our founding, we have remained committed to our strategy of achieving “Continuous Transformational Growth” through M&A in the entertainment industry. By strictly adhering to the discipline of executing only M&A transactions that are EPS-accretive, we have successfully achieved growth that has, as a whole, exceeded our initial expectations.

(Source: page 8 of “FY2026/1 3Q Earnings Presentation” disclosed on December 12, 2025)

That said, because we prioritized the speed of our M&A execution, we conducted public offerings to secure M&A standby funds for two consecutive years. By strictly maintaining our M&A discipline, we achieved a 196% increase in projected net income before amortization of goodwill for the next fiscal year, despite a 48% increase in the number of shares outstanding since our IPO. Consequently, our Cash EPS is expected to grow by 101%, effectively doubling. However, if we had continued with this strategy, a series of public offerings would have been unavoidable.

What we miscalculated was that the cost of continuous public offerings – specifically, the resulting short-term supply-demand concerns – was far heavier than we had imagined. Especially, we now recognize that for investors with shorter time horizons, the uncertainty of “not knowing when the next offering might occur” acted as a barrier to new purchases, effectively capping our share price performance.

We take this lack of foresight very seriously, and it is based on this deep reflection that we have decided to present this strategic revision.

(Source: page 9 of “FY2026/1 3Q Earnings Presentation” disclosed on December 12, 2025)

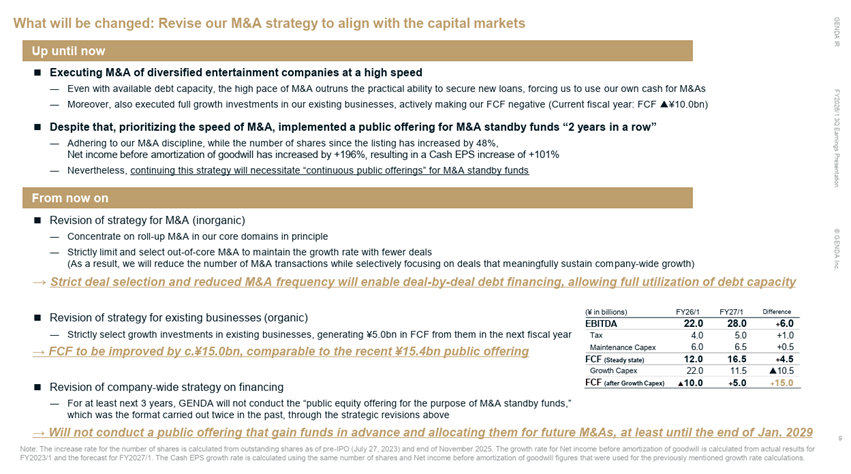

First and foremost, what will remain unchanged is our commitment to achieving “Continuous Transformational Growth” through M&A in the entertainment industry. Furthermore, we will continue to execute only those M&A transactions that are EPS-accretive. We will steadfastly uphold these core strategic principles moving forward.

At the same time, we are refining our M&A strategy to be more aligned with the expectations of the capital markets. Specifically, we will implement changes in the following three areas:

First is the company-wide strategic shift regarding public offerings. We have established a policy that we will not conduct any “public offerings for the purpose of securing M&A standby funds” – a practice we carried out twice in the past – for at least the next three years.

Second is the shift in our M&A strategy. Regarding our future M&A, we will, in principle, focus on roll-up M&A within our core business domains. Conversely, M&A outside of these core areas will be limited and highly selective. As a result, while we expect the total number of M&A transactions to decrease, we will ensure each deal is strictly chosen for its ability to sustain and drive our overall growth.

Third is the strategic shift in our existing businesses. By being more selective with our growth investments in existing operations, we aim to generate 5.0 billion yen in FCF from these businesses in the next fiscal year.

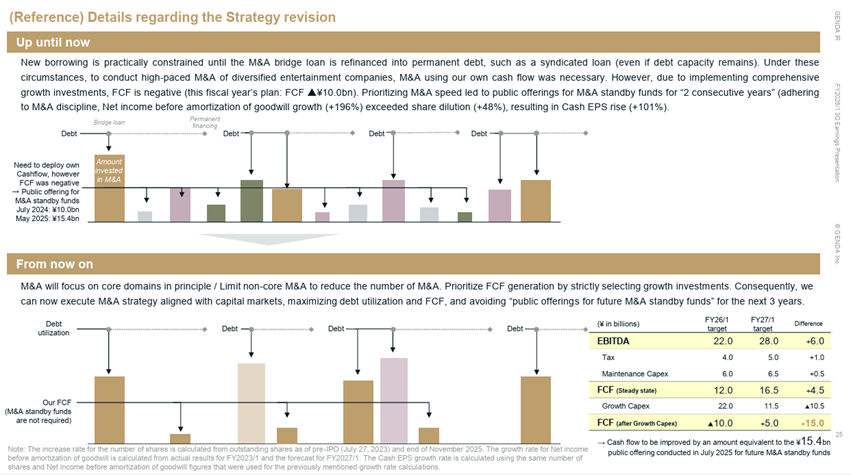

Until now, we have executed M&A at a rapid pace across a diverse range of entertainment companies. In practice, our new financing could not keep pace with such a high volume of deals despite our remaining debt capacity, necessitating the use of our own cash reserves. Simultaneously, we were aggressively reinvesting in our existing businesses for comprehensive growth, as detailed below, which resulted in a deliberate negative Free Cash Flow (FCF).

(Source: page 25 of “FY2026/1 3Q Earnings Presentation” disclosed on December 12, 2025)

As shown in the table on the bottom right, after paying taxes and maintenance Capex, we are currently in a position to generate approximately 16.5 billion yen in annual FCF if we were to suspend our growth Capex. At the same time, we believe there are still business segments where we should not yet halt our growth investments, and they are primarily located in North America.

By deploying growth investments from our baseline FCF of 16.5 billion yen, we aim to generate a final FCF of 5.0 billion yen in the next fiscal year. This represents an improvement of approximately 15.0 billion yen in FCF compared to the current fiscal year. Notably, this improvement is on par with the 15.4 billion yen raised in our most recent public offering for M&A standby funds. Through these strategic updates, we believe we can sustain the same growth rate without conducting any public offerings aimed at pre-funding for M&A, at least until the end of January 2029.