We intend to issue corporate bonds (straight bonds) as soon as we are ready. While we will start with small amount (5.0 billion to 10.0 billion) as we need to discover bond investors’ demand as Debt IPO, we expect to issue regularly after terms and conditions for the initial bond are determined.

In addition, the advantages of direct financing (corporate bonds) compared to indirect financing (bank loans) are as follows.

(i) “More robust” financing is ensured by market principles.

In the case of banks, it is often the case that even if the borrowing rate is raised, the loan approval is not granted in the first place. On the other hand, in the case of direct financing, which provides access to funds from all over the world, raising the borrowing rate basically makes it possible to raise funds (on the same level as investors’ risk-return metrics).

At this time, we do not expect interest rates to rise significantly for our individual reasons, however, we believe that, in theory, it would be desirable for banks and other financial institutions, as well as for our shareholders, to be able to raise funds even more solidly as described above.

(ii) The direct market focuses on our strength, “cash flow.”

Direct financing tends to look more at cash flow as a source of funding compared to indirect financing.

Since we are a growing company in the eighth year since the establishment, the absolute amount of our “net assets,” which is greatly affected by the “number of years” we have been accumulating earnings, is not large when compared to matured companies.

On the other hand, our mainstays, operation business of amusement arcades and karaoke businesses, enable us to generate stable cash flow.

Indicators focusing on “net assets” are indicators of “how much can be recouped in the event of bankruptcy” (e.g., capital adequacy ratio and debt equity ratio). On the other hand, indicators centered on “cash flow” are indicators of “whether the company will go bankrupt in the first place” (e.g., Net Debt / EBITDA).

While we keep monitoring BS indicators such as capital adequacy ratio, etc., by leveraging our ability to generate cash flow and diversifying our fundraising, we would like to ensure stable financing, furthermore, make further continuous M&A possible and bring transformational growth to our shareholders.

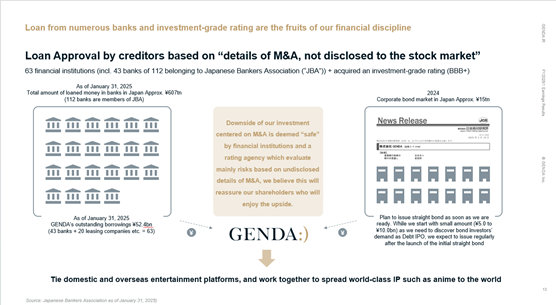

In addition, we have successfully obtained indirect financing from 63 financial institutions, including 43 of the 112 banks which belong to Japanese Bankers Association. In addition to this, we received an external rating of investment grade, “BBB+” this time.

We believe the key to this is that we have passed creditor’s evaluations based on “detailed materials of M&A that are not disclosed to the stock market.”

Downside of our investment centered on M&A is deemed “safe” by financial institutions and a rating agency which evaluate mainly risks based on undisclosed details of M&A, we believe this will reassure our shareholders who will enjoy the upside.

For details, please refer to page 13 of “FY2025/1 Full-year Earnings Presentation” disclosed on March 12, 2025, and “Q1. What are your intentions regarding the acquisition of a new credit rating from Japan Credit Rating Agency, Ltd. (“JCR”)?” in the “Frequently Asked Questions and Answers (February 2025)” disclosed on February 28, 2025.