Company Information

Some sections of MSCI’s website regarding our company have been updated to reflect our actual business status, reporting a gambling-related revenue ratio of 0.17%. However, as certain other pages still incorrectly show a range of 5 to 9.9%, we are continuing to request that these errors be corrected as soon as possible.

(Repost: Q4 of “Frequently Asked Questions and Answers (November 2025)” disclosed on November 27, 2025)

We formally contacted MSCI with a request for correction on October 31, 2025, upon the disclosure of the “Frequently Asked Questions and Answers” on the same day, which was the date we, as a company, officially disclosed the revenue from our amusement poker business (approximately 0.2 billion yen per year ÷ Revenue of 111.7 billion yen for the fiscal year ending on January 31, 2025 = approximately 0.1%).

However, as the incorrect information stating 5% to 9.9% is still stated at present, we are currently continuing to request the quickest possible correction.

The timeline is as follows.

October 31: GENDA formally requested MSCI for correction on the same day we disclosed the “Frequently Asked Questions and Answers.”

November 3: MSCI contacted us, stating the information provided lacked sufficient detail.

November 5: GENDA submitted monthly sales data for the amusement poker business to MSCI.

November 21: The amusement poker revenue data we had submitted was added to our company’s page on MSCI. However, the gambling revenue ratio remains listed as 5 to 9.9%.

November 21: GENDA requested MSCI to correct the erroneous gambling revenue ratio once again.

As of today: Awaiting MSCI’s response.

The incorrect listing of our amusement poker business’s revenue ratio on MSCI has resulted in a situation where some institutional investors, who otherwise would have been considering purchasing our company’s shares, are currently finding it difficult to execute purchases due to restrictions in their investment mandates.

We will strive to ensure that the capital market, including MSCI, accurately understands our company’s business activities.

In addition to the aforementioned situation, we have taken the following actions.

From November 25 to December 9: GENDA conducted four rounds of continuous follow-up with MSCI.

December 16: Due to the lack of response from MSCI, GENDA escalated the matter by reaching out through a different channel than before.

December 24: Due to the lack of response from MSCI, GENDA followed up again through multiple channels, including email and direct phone calls.

MSCI updated certain pages regarding our company and notified GENDA of the change.

GENDA requested MSCI to ensure accurate information is reflected across all relevant pages.

MSCI responded that they will correct the information on all pages as soon as possible.

December 26: GENDA has strongly requested MSCI to promptly correct the pages that remain inaccurate. We will maintain continuous communication with MSCI and all other capital market participants to ensure an accurate understanding of our business activities.

M&A Strategy

To summarize our position: there is absolutely no change to the core of our strategy – achieving “Transformational growth through continuous M&A” – nor to our discipline of pursuing “M&A that contributes to EPS improvement.”

Building on this foundation, we have announced a “shift toward an M&A strategy aligned with the capital markets,” and have committed to not conducting any “public offerings for the purpose of securing M&A standby funds” until at least the end of January 2029.

(Source: page 6 of “FY2026/1 3Q Earnings Presentation” disclosed on December 12, 2025)

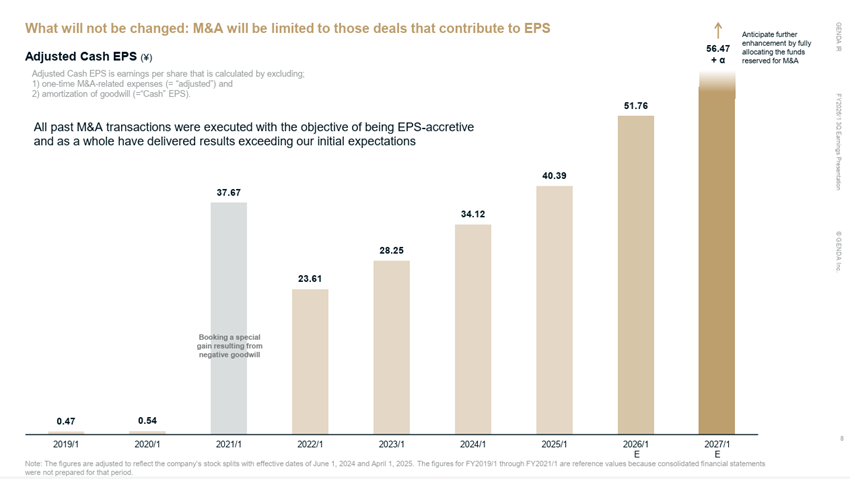

Since our founding, we have remained committed to our strategy of achieving “Continuous Transformational Growth” through M&A in the entertainment industry. By strictly adhering to the discipline of executing only M&A transactions that are EPS-accretive, we have successfully achieved growth that has, as a whole, exceeded our initial expectations.

(Source: page 8 of “FY2026/1 3Q Earnings Presentation” disclosed on December 12, 2025)

That said, because we prioritized the speed of our M&A execution, we conducted public offerings to secure M&A standby funds for two consecutive years. By strictly maintaining our M&A discipline, we achieved a 196% increase in projected net income before amortization of goodwill for the next fiscal year, despite a 48% increase in the number of shares outstanding since our IPO. Consequently, our Cash EPS is expected to grow by 101%, effectively doubling. However, if we had continued with this strategy, a series of public offerings would have been unavoidable.

What we miscalculated was that the cost of continuous public offerings – specifically, the resulting short-term supply-demand concerns – was far heavier than we had imagined. Especially, we now recognize that for investors with shorter time horizons, the uncertainty of “not knowing when the next offering might occur” acted as a barrier to new purchases, effectively capping our share price performance.

We take this lack of foresight very seriously, and it is based on this deep reflection that we have decided to present this strategic revision.

(Source: page 9 of “FY2026/1 3Q Earnings Presentation” disclosed on December 12, 2025)

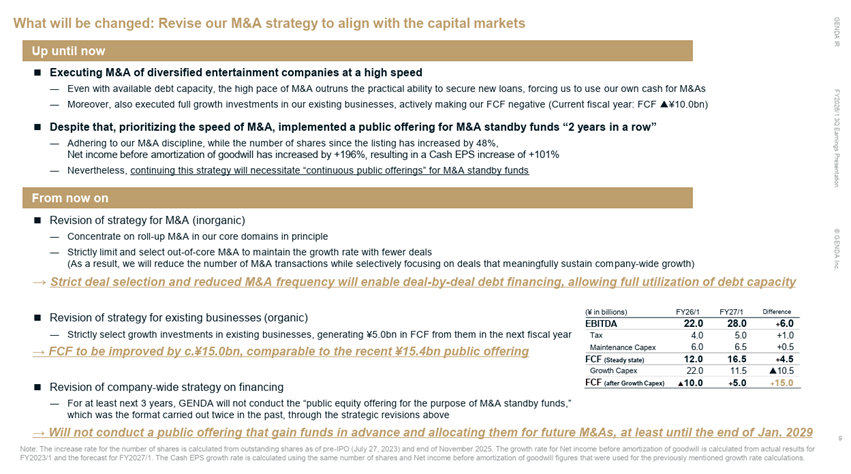

First and foremost, what will remain unchanged is our commitment to achieving “Continuous Transformational Growth” through M&A in the entertainment industry. Furthermore, we will continue to execute only those M&A transactions that are EPS-accretive. We will steadfastly uphold these core strategic principles moving forward.

At the same time, we are refining our M&A strategy to be more aligned with the expectations of the capital markets. Specifically, we will implement changes in the following three areas:

First is the company-wide strategic shift regarding public offerings. We have established a policy that we will not conduct any “public offerings for the purpose of securing M&A standby funds” – a practice we carried out twice in the past – for at least the next three years.

Second is the shift in our M&A strategy. Regarding our future M&A, we will, in principle, focus on roll-up M&A within our core business domains. Conversely, M&A outside of these core areas will be limited and highly selective. As a result, while we expect the total number of M&A transactions to decrease, we will ensure each deal is strictly chosen for its ability to sustain and drive our overall growth.

Third is the strategic shift in our existing businesses. By being more selective with our growth investments in existing operations, we aim to generate 5.0 billion yen in FCF from these businesses in the next fiscal year.

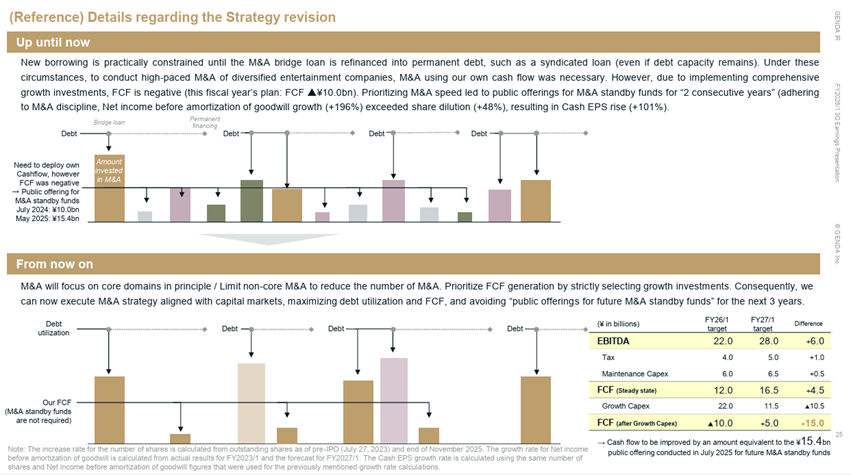

Until now, we have executed M&A at a rapid pace across a diverse range of entertainment companies. In practice, our new financing could not keep pace with such a high volume of deals despite our remaining debt capacity, necessitating the use of our own cash reserves. Simultaneously, we were aggressively reinvesting in our existing businesses for comprehensive growth, as detailed below, which resulted in a deliberate negative Free Cash Flow (FCF).

(Source: page 25 of “FY2026/1 3Q Earnings Presentation” disclosed on December 12, 2025)

As shown in the table on the bottom right, after paying taxes and maintenance Capex, we are currently in a position to generate approximately 16.5 billion yen in annual FCF if we were to suspend our growth Capex. At the same time, we believe there are still business segments where we should not yet halt our growth investments, and they are primarily located in North America.

By deploying growth investments from our baseline FCF of 16.5 billion yen, we aim to generate a final FCF of 5.0 billion yen in the next fiscal year. This represents an improvement of approximately 15.0 billion yen in FCF compared to the current fiscal year. Notably, this improvement is on par with the 15.4 billion yen raised in our most recent public offering for M&A standby funds. Through these strategic updates, we believe we can sustain the same growth rate without conducting any public offerings aimed at pre-funding for M&A, at least until the end of January 2029.

Financial Results

Whether or not to disclose the results of an extraordinary financial closing is at the discretion of each company under Tokyo Stock Exchange disclosure rules. For the reasons outlined below, we have decided to refrain from making a public announcement at this time.

For our company, share repurchases are not intended as a shareholder return; rather, they represent strategic procurement within our M&A strategy. Our goal is to secure capital at an attractive valuation to be utilized as consideration for future “stock-deal M&A.” Announcing the implementation of an extraordinary financial closing would signal the specific timing of our share repurchases to the market. Consequently, this poses a risk of inducing speculative trading by third parties. Therefore, we believe that refraining from disclosing the specific timing of acquisitions to ensure efficient share repurchases will contribute to the maximization of shareholder value over the medium to long term.

Business

It is a fact that the performance of our North American operations has fallen behind our initial projections, and we take this situation very seriously. We would like to take this opportunity to re-explain the factors behind this delay and the specific countermeasures we are currently implementing.

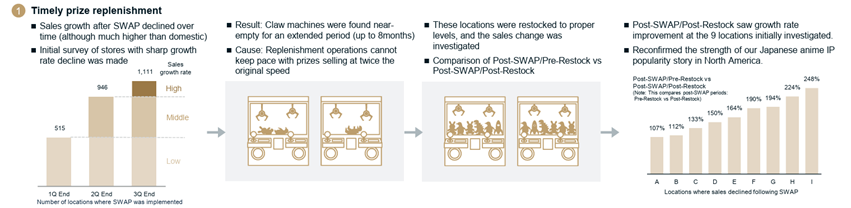

First, our initial hypothesis that Japanese anime IP prizes would see strong demand in North America yielded results beyond our expectations. However, we discovered that on-site replenishment could not keep pace with the speed at which these prizes were being cleared.

Upon implementing proper restock procedures at the affected locations, we confirmed a significant turnaround, with growth rates improving by as much as 248%. Having reaffirmed the robust demand for Japanese anime IP in North America, we have launched measures to normalize this replenishment cycle as quickly as possible.

(Source: page 16 of “FY2026/1 3Q Earnings Presentation” disclosed on December 12, 2025)

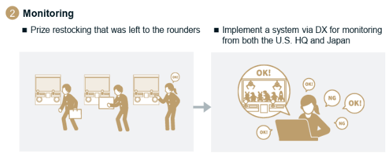

First, we will introduce DX solutions to bring full visibility to prize replenishment and inventory management, which were previously left to the discretion of individual rounder. This will allow us to establish a robust system where both the U.S. headquarter and Japan can monitor and track the real-time operational status of every location.

(Source: page 16 of “FY2026/1 3Q Earnings Presentation” disclosed on December 12, 2025)

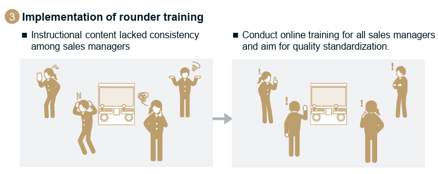

In addition, we have been conducting online training sessions for all sales managers responsible for rounders. By standardizing our guidance and management criteria, we aim to elevate the operational quality across the entire organization.

(Source: page 16 of “FY2026/1 3Q Earnings Presentation” disclosed on December 12, 2025)

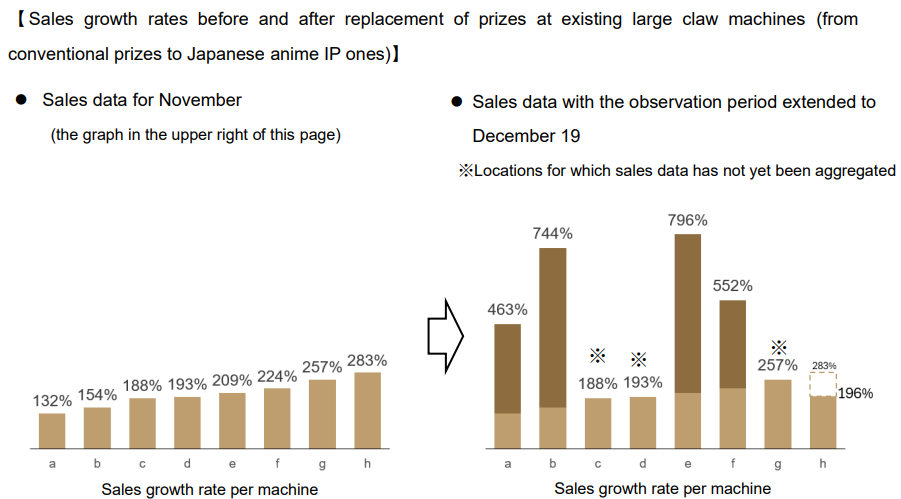

Additionally, regarding our PMI initiatives utilizing existing claw machines, current performance is outpacing the results announced in our third quarter earnings announcement. We would like to share these figures with you on a preliminary basis.

In our third quarter earnings announcement, we disclosed the “sales growth rates for locations where we maintained existing claw machines but refreshed the prizes with Japanese anime IP,” as shown in the graph below. This initiative is straightforward: while the machines themselves remain the same, we simply replace conventional prizes with Japanese anime IP ones.

(Source: page 17 of “FY2026/1 3Q Earnings Presentation” disclosed on December 12, 2025)

Subsequently, an analysis of sales data – with the observation period extended to December 19 – confirmed further growth at the same locations.

This initiative offers superior investment efficiency because it drives sales growth with zero capital investment; it requires no machine replacement and the prizes are recorded as cost of goods sold rather than Capex. Our conventional SWAP initiative involved Capex for replacing machines, which limited their implementation to high-efficiency locations. In contrast, this new approach achieves growth through prize replacement alone, allowing us to scale it across all locations.

The feasibility of this initiative is rooted in the expansion of our business scale through roll-up M&A of mini-locations in North America. This growth has significantly enhanced our procurement power, enabling us to secure not only conventional small prizes but also large-scale Japanese anime IP prizes.

To ensure we capture the demand of the current holiday season, we are working diligently to maximize our financial performance in tandem with the aforementioned operational improvements.

Stock Information

How should investors understand Zennor’s large shareholding report submitted on December 24, 2025?

Zennor has been a shareholder in GENDA since our IPO, having invested from the first day of listing based on alignment with the Company’s long-term equity story, including our roll-up M&A strategy centered on business succession.

Accordingly, Zennor is not a new shareholder, but rather an investor who has held a position since our IPO; its recent additional purchase of our shares resulted in the filing of a large shareholding disclosure.

Since the IPO, GENDA has maintained ongoing dialogue with Zennor – both in person and online – as part of our regular engagement with long-term institutional investors, discussing the progress and execution of our strategy.

Zennor has consistently expressed support for GENDA’s roll-up M&A strategy, with its focus on business succession, and continues to engage with the Company as a long-term investor.

According to Zennor’s large shareholding disclosures, Zennor increased its ownership materially beginning immediately after the announcement of our third quarter results, including an increase of approximately 0.93% on the first trading day following the earnings release (December 15).

GENDA views this timing as indicative of a positive response to the Company’s refined M&A policy, which was updated to ensure greater alignment with capital market expectations, alongside an assessment that the Company’s valuation level had become attractive.

As a result, from GENDA’s perspective, Zennor’s investment approach is understood to be that of a long-term, conviction-based shareholder, rather than that of an activist investor.

Regarding the status of our share repurchase program, we will provide monthly updates through timely disclosures and “Report on Share Repurchase.”

The initial disclosure, covering purchases made in December 2025, is scheduled for release by January 15, 2026, in compliance with relevant laws and regulations. Please refer to TDnet, EDINET, or our IR website for the latest information.

Our IR website https://genda.jp/en/ir/

Although a decrease in Midas Capital’s ownership “ratio” has been reported, there has been no change in the actual “number of shares” held by them.

This decrease is solely due to an increase in our total shares outstanding following the share exchange with CARATT, Inc. Our understanding remains that Midas Capital maintains its policy of holding our shares over the ultra-long term.