Company Information

We will use all means at our disposal to maintain a good relationship with our shareholders and investors and continue our efforts to enhance our enterprise value and equity value. On this basis, we ask for the continued understanding and support of all our stakeholders. The following is based on the answers to the above questions in the minutes of the financial results briefing. We include it in this monthly FAQs as well to inform everyone.

With a background of having established a certain strategy as a M&A enterprise and entering a new growth phase to execute this cycle toward the future, GENDA has decided to change to the most appropriate management structure from the viewpoint of executing the cycle at the fastest speed.

As a result, we have decided that Mai Shin will step down as Representative Director and President at the next General Meeting of Shareholders, to be succeeded by Nao Kataoka, the co-founder of the company, and at the same time, Taiju Watanabe, incumbent Director CFO, and Kohei Habara, incumbent Director CSO, will be appointed as Managing Director.

Shin, who is Representative Director, recognizes that it is important to avoid making the organization rigid and metabolize the management structure to grow sustainably and increase the enterprise value. She has believed from a long-term perspective that it is important to promote the transfer of the management at the right timing for the development of an organization.

At the start of the third fiscal year after we went public in July 2023, while the M&A pipeline is the largest ever in terms of value and further acceleration of growth is anticipated under the unchanged strategy, she believed that we should change the leadership in the time of business strength.

With both the business environment and performance in very good shape, she decided to change President to Kataoka, her co-founder, at this timing, and pass the torch to Watanabe and Habara, who have been leading the whole company and GENDA’s growth in line with Kataoka, and provide rearguard support to the management as a director.

Under the new structure with Kataoka as Representative Director and President, we will once again seriously aim to become the world’s No. 1 entertainment company by 2040.

This definition of the world’s No. 1 entertainment company aims to be the world’s No.1 in the entertainment industry in terms of revenue, EBITDA, market capitalization, and all their indicators.

GENDA ended its seventh fiscal year in very good shape, both in terms of organic growth and M&A growth. We believe that we have been able to embody the conglomerate premium of the entertainment industry, where the entertainment is contiguous, and the same group management can grow through synergies rather than stand alone.

Besides, the entertainment industry has also grown in tandem with the increase in human leisure time, in which Japan’s world-class anime IP culture has taken root globally.

In the future, many Japanese entertainment companies will not fight domestically in Japan but will work together in the same direction and spread their wings to the world.

GENDA is now playing the role of a platform, which is the bridge, through roll-up M&A. In the mid- to long-term, we seriously aim to become a leading entertainment company in Japan, including the IP field, and ultimately to become the world’s No. 1entertainment company originating from Japan.

With 15 years to go until 2040, we will do our utmost to make life more fun for your days. We would be very grateful if you could kindly support us in the long term.

Over the years, Ms Hayashi has produced many works in the entertainment industry based on her keen perspective of the times and deep insight into society.

We are confident that her outstanding creativity and ability to convey messages will provide us with important insights in our goal of creating entertainment that “increases the total amount of fun.”

In addition, Ms Hayashi has connections not only with the publishing industry, but also with prominent figures and companies in a wide variety of fields. We hope that Ms Hayashi’s participation will create new opportunities for us to collaborate with companies we have not been able to approach in the past and to discover new information.

Mariko Hayashi (Mariko Togo) born on April 1, 1954

Newly appointed, outside, independent

January 1986 Won the 94th Naoki Prize for “The Last Flight Home” and “To Kyoto”

January 2011 Won Chevalier de la Legion d’Honneur

November 2018 Won Medal with Purple Ribbon

May 2020 President, Japan Writers’ Association (present)

December 2020 Won Kan Kikuchi Award

July 2022 Chairperson of the Board of Trustees, Nihon University (present)

Financial Results

We intend to issue corporate bonds (straight bonds) as soon as we are ready. While we will start with small amount (5.0 billion to 10.0 billion) as we need to discover bond investors’ demand as Debt IPO, we expect to issue regularly after terms and conditions for the initial bond are determined.

In addition, the advantages of direct financing (corporate bonds) compared to indirect financing (bank loans) are as follows.

(i) “More robust” financing is ensured by market principles.

In the case of banks, it is often the case that even if the borrowing rate is raised, the loan approval is not granted in the first place. On the other hand, in the case of direct financing, which provides access to funds from all over the world, raising the borrowing rate basically makes it possible to raise funds (on the same level as investors’ risk-return metrics).

At this time, we do not expect interest rates to rise significantly for our individual reasons, however, we believe that, in theory, it would be desirable for banks and other financial institutions, as well as for our shareholders, to be able to raise funds even more solidly as described above.

(ii) The direct market focuses on our strength, “cash flow.”

Direct financing tends to look more at cash flow as a source of funding compared to indirect financing.

Since we are a growing company in the eighth year since the establishment, the absolute amount of our “net assets,” which is greatly affected by the “number of years” we have been accumulating earnings, is not large when compared to matured companies.

On the other hand, our mainstays, operation business of amusement arcades and karaoke businesses, enable us to generate stable cash flow.

Indicators focusing on “net assets” are indicators of “how much can be recouped in the event of bankruptcy” (e.g., capital adequacy ratio and debt equity ratio). On the other hand, indicators centered on “cash flow” are indicators of “whether the company will go bankrupt in the first place” (e.g., Net Debt / EBITDA).

While we keep monitoring BS indicators such as capital adequacy ratio, etc., by leveraging our ability to generate cash flow and diversifying our fundraising, we would like to ensure stable financing, furthermore, make further continuous M&A possible and bring transformational growth to our shareholders.

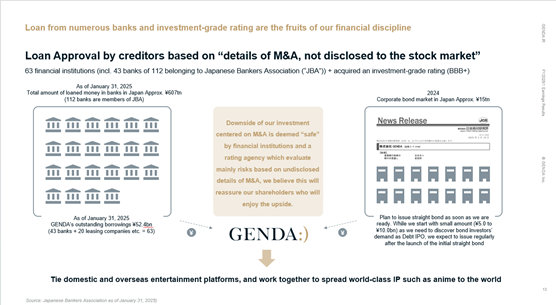

In addition, we have successfully obtained indirect financing from 63 financial institutions, including 43 of the 112 banks which belong to Japanese Bankers Association. In addition to this, we received an external rating of investment grade, “BBB+” this time.

We believe the key to this is that we have passed creditor’s evaluations based on “detailed materials of M&A that are not disclosed to the stock market.”

Downside of our investment centered on M&A is deemed “safe” by financial institutions and a rating agency which evaluate mainly risks based on undisclosed details of M&A, we believe this will reassure our shareholders who will enjoy the upside.

For details, please refer to page 13 of “FY2025/1 Full-year Earnings Presentation” disclosed on March 12, 2025, and “Q1. What are your intentions regarding the acquisition of a new credit rating from Japan Credit Rating Agency, Ltd. (“JCR”)?” in the “Frequently Asked Questions and Answers (February 2025)” disclosed on February 28, 2025.

Stock Information

The conclusion is that we do not conduct a stock lending transaction.

The conclusion is as stated above. However, since we presume that we have received an inquiry that “Isn’t the management team conducting a stock lending transaction?” because of the following disclosure, we would like to explain this.

∙ Change Report on the Report of Possession of Large Volume of Mai Shin, Representative Director and President, filed on January 29, 2025.

“Regarding 920,000 shares collateralized to Tokai Tokyo Securities Co., Ltd. on January 30, 2024, I rescinded the collateral (release of pledge) on March 4, 2025, and lent 920,000 shares to Tokai Tokyo Securities Co., Ltd. based on a loan agreement on March 4, 2025. The name and the voting right of the loaned shares concerned are possessed by Shin Mai LLC.”

∙ Change Report on the Report of Possession of Large Volume of Nao Kataoka, Representative Director and Chairman of the Board, filed on February 20, 2025.

“Regarding 920,000 shares collateralized to Tokai Tokyo Securities Co., Ltd. on January 30, 2024, I rescinded the collateral (release of pledge) on February 17, 2025, and lent 920,000 shares to Tokai Tokyo Securities Co., Ltd. based on a loan agreement on February 17, 2025. The name and the voting right of the loaned shares concerned are possessed by Nao Kataoka.”

The above is an administrative disclosure associated with the switch from “a share collateral loan agreement” in which a shareholder pledges shares he or she possesses as a collateral to financial institutions to obtain a loan to “a loan agreement.”

Under the “loan agreement,” although the ownership of the shares is transferred from Shin and Kataoka to Tokai Tokyo Securities Co., Ltd., the names and the voting rights remain with Kataoka and Shin because Tokai Tokyo Securities Co., Ltd., which is the owner, made a “special shareholder request.”

Besides, although Tokai Tokyo Securities Co., Ltd. pledges the shares it owns to call loan brokers as further collateral, it cannot offer the shares to a third party as lending stock because the voting rights belong to the original shareholders (Shin and Kataoka in this case).

Therefore, it is not correct to speculate that the said agreement “may have resulted in an increase in lending stock and an increase in short selling.”

In addition, as mentioned at the beginning, since our management team does not conduct a stock lending transaction in the first place, short selling in the market is not due to stock lending by our management team.

Meanwhile, let us explain our approach to short selling.

For a start-up enterprise like us, we believe that it is essential to maintain the liquidity, or maintain the intraday trading volume, to survive in the capital markets.

This is because without liquidity, institutional investors would not be able to buy our shares even if they wanted to buy new ones.

This is because, since institutional investors invest a large amount of money, unlike individual ones, the minimum investment amount for a single company is inevitably large. Therefore, if the liquidity is low, they will have a problem that the share price drastically goes up in the process of buying or drastically goes down when they sell.

In addition, because M&A does not always occur every quarter, for example, the effect of transformational growth is not seen with every short-term announcement of financial results, but only with long-term announcement of M&A and each PMI.

As a result, our shares are held primarily by investors who prefer to hold them for the long term. This investor base is an important foundation that supports our long-term growth strategy, however, it also makes the diminishing trend of liquidity an inevitable phenomenon.

At first glance, short selling may appear to have a negative impact on the market. However, it is only short-term. Since short selling is subject to repurchase obligations, it will be eliminated in the long term and return to neutral. On the other hand, liquidity will certainly improve in the meantime. From this perspective, we think that short selling has a certain significance because it contributes to this improvement in liquidity.

Finally, we will continue to closely monitor various concerns related to short selling, stock lending, and stock liquidity issues and seek appropriate measures to address them.

We made a total of 71 timely disclosures, including M&A and monthly FAQs, and provided IR to a cumulative number of 185 domestic and 210 overseas institutional investors as well as individual shareholders in 2024. We have made efforts to deepen their understanding of our business conditions, strategies and growth potential, and aim to strengthen the relationship of trust with them and create better enterprise value and equity value.

In the process, we will keep responding while facing various challenges, and strive to contribute to the growth of our company and the healthy development of the market through our efforts on them. We would be grateful for your continued support.

-

Frequently Asked Questions and Answers (June 2026)

-

Frequently Asked Questions and Answers (May 2026)

-

Frequently Asked Questions and Answers (April 2026)

-

Frequently Asked Questions and Answers (March 2026)

-

Frequently Asked Questions and Answers (February 2026)

-

Frequently Asked Questions and Answers (January 2026)